So you’ve heard the buzzword “startup studio,” but what exactly does it mean to be a startup studio? Here are the answers you need about why startup studios are becoming a popular model for entrepreneurial success and how this trend is changing corporate innovation.

What is a Startup Studio?

Startup Studio Insider defines a startup studio as an organization that provides investment, resources, and guidance to startups in order to build and launch successful startups in various industries. Some people call it a venture studio, others call it a startup factory or startup studio. No matter what you call it, this startup model is quickly gaining traction in helping launch startups everywhere.

Startup studios allow founders to focus all their time and energy on developing every aspect behind their business idea, while studios are dedicated to minimizing any challenges that come along the way. By offering a wide range of resources, industry knowledge, and the funding required to build, launch, and support a startup (even after post-launch), startup studios are becoming a game-changing solution for rising startups.

From Atomic to Wilbur Labs and eFounders, numerous startups are being built around the world and gaining major traction along the way. Deciding the best path to found and build a company can be a daunting task. To help you understand the unique offerings of startup studios, here are some of the most important benefits startup studios offer:

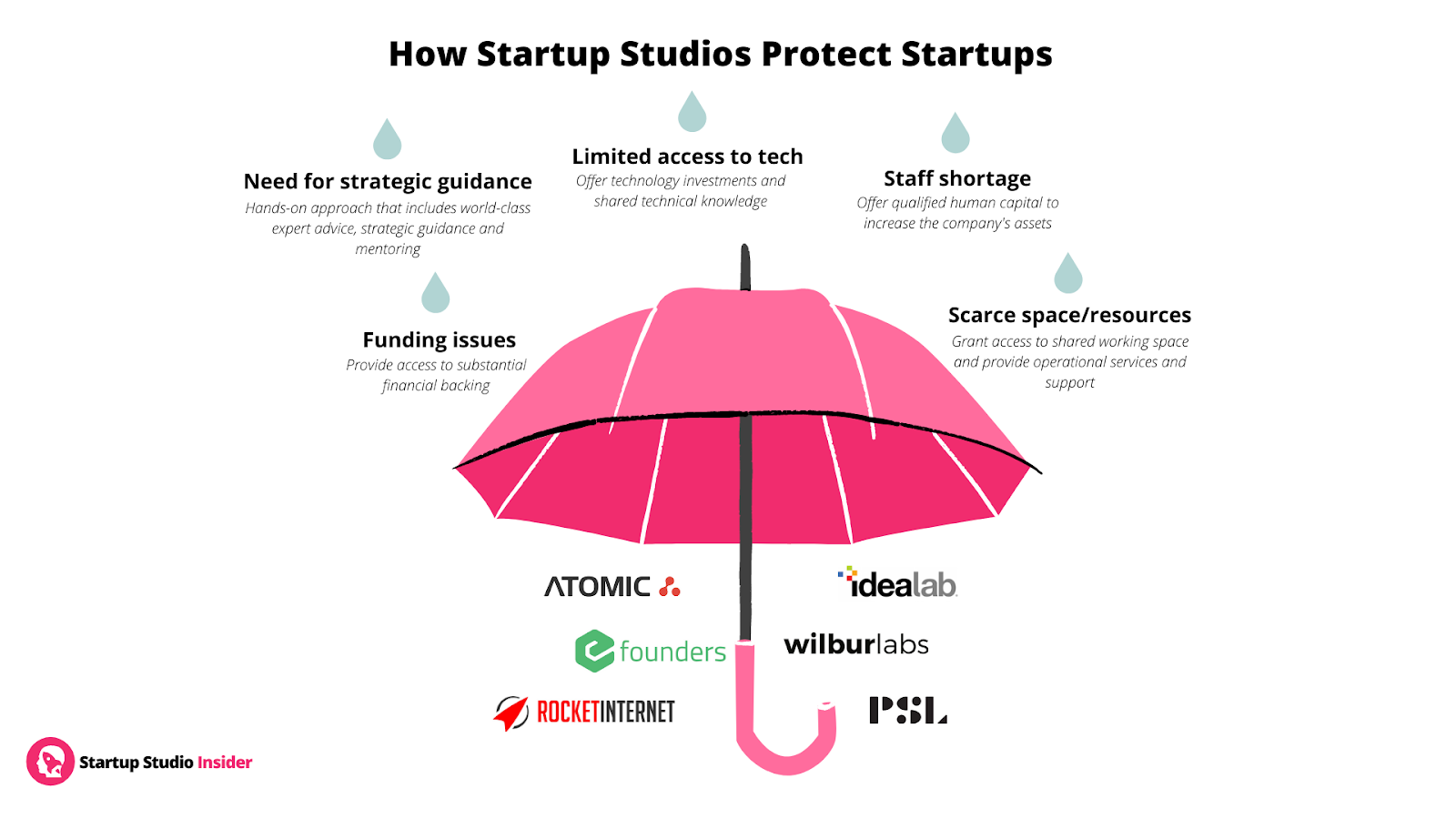

How Startup Studios Protect Startups – Graphic by Startup Studio Insider

- Strategic Counsel

Startup entrepreneurs oftentimes lack the necessary experience to anticipate the roadblocks that come along with building a business. In addition, the expertise level of a founder doesn’t always cover all grounds including marketing knowledge, product development, testing, and research. That is not a problem for startup studios, as they provide a wide spectrum of tools and resources to build a perfect strategic plan. In addition, studios have access to a wealth of knowledge in technology tools and trends, business operations, human resources, and more, which become part of their core team to help startups succeed.

- Core and Shared Resources

Out of all the investment platforms, studios take the most hands-on approach and provide the most resources. With this, startup studios are able to provide access to the largest amount of top-notch resources to help enhance the vision and goals of the startup and cut down the launch time that could usually take a couple of years to about three months.

- Human Capital

Usually, the vast majority of startup companies are made up of small teams. This is why getting the perfect fit to support the launch and operations needs of your business is crucial. Startup studios help tackle this problem by recruiting the right team with diverse backgrounds and broad skills to handle the immense workload that comes with the challenge of launching a startup.

- Funding

Building a startup from the ground off can be exhausting and cash-consuming. What frequently goes wrong is that startup management fails to achieve the next milestone before cash is exhausted. Startup studios are able to solve this problem by refining the needs and expenses required to prepare for the launch and avoid the risk of becoming insolvent by providing funds even after post-launch. This is one of the major differentiating factors of startup studios compared to their competitor founding models out there.

- In-Depth Market Research

According to Startup Studio Insider, startup studios are highly selective, and as a result, will not launch a startup without substantial research and data to prove that there is a market and potential for success. This in-depth market research ultimately leads to better decisions when preparing for the launch and can help mitigate any risks in the long run.